Canned Vegetables Market Size

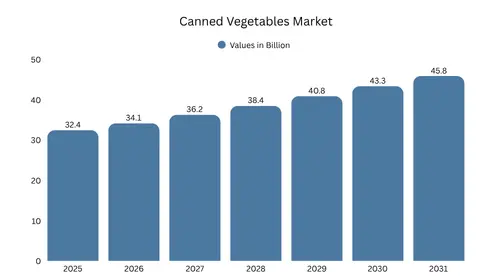

According to Zeal Market Research, the global canned vegetables market size was valued at USD 32.4 billion in 2025 and is projected to grow from USD 34.1 billion in 2026 to reach USD 45.8 billion by 2031, registering a CAGR of 6.1% during the forecast period (2026-2031). The canned vegetables market growth is driven by rising demand for shelf-stable food products that offer long storage life without refrigeration, making them suitable for both developed and developing markets. Increasing urbanization, dual-income households, and time-constrained lifestyles are accelerating reliance on ready-to-use ingredients. In addition, improvements in canning processes, such as high-temperature short-time sterilization, are preserving nutritional content while ensuring food safety.

Key Market Insights

- North America accounted for the leading regional share of the global canned vegetables market at 34.2% in 2025, supported by high per capita consumption of processed foods and strong penetration of private label products.

- By product type, canned tomatoes led the market in 2025 with 28.5% of global revenue, equivalent to approximately USD 9.2 billion, due to extensive use in sauces, ready meals, and food processing applications.

- Metal cans dominated packaging due to their superior barrier properties against light, oxygen, and contaminants, ensuring extended shelf life and minimal spoilage.

- Supermarkets and hypermarkets remained the primary distribution channel, benefiting from bulk purchasing behavior, in-store promotions, and wide product assortment.

- The foodservice segment is witnessing steady growth as restaurants and institutional buyers prefer standardized, pre-processed ingredients to reduce preparation time and operational costs.

What are the growth factors for the canned vegetables market?

Rising Demand in Emerging Economies

Emerging economies are presenting high-growth potential due to the rapid expansion of urban centers and increasing exposure to modern retail formats such as supermarkets, hypermarkets, and organized grocery chains. Rising disposable income levels and a growing middle-class population are shifting consumption patterns toward packaged and shelf-stable food products. Changing dietary habits, including increased reliance on convenient meal solutions, are further accelerating adoption. Government initiatives focused on food security, supply chain efficiency, and reduction of post-harvest losses are supporting the use of preservation techniques such as canning. Additionally, improvements in cold chain limitations in developing regions make canned vegetables a practical alternative to fresh produce. Local manufacturers are also entering the market with competitively priced offerings tailored to regional cuisines, strengthening market penetration.

Product Innovation and Clean Label Trends

There is a strong shift toward clean-label canned vegetables, with manufacturers actively reformulating products to reduce sodium content, eliminate artificial preservatives, and remove synthetic additives. Organic-certified, non-GMO, and minimally processed variants are gaining traction, particularly among health-conscious consumers. Product innovation is extending to ready-to-eat seasoned vegetables, mixed vegetable combinations, and fortified offerings with added vitamins and minerals to enhance nutritional value. Transparent labeling, ingredient traceability, and compliance with stringent food safety standards are becoming critical purchasing factors. This trend is especially prominent in North America and Europe, where regulatory oversight and consumer awareness are high, driving manufacturers to differentiate through quality and transparency.

Expansion of Private Label Brands

Private label expansion is reshaping competitive dynamics within the canned vegetables market. Large retail chains are leveraging their procurement capabilities, supplier networks, and economies of scale to offer high-quality products at competitive price points. These products are increasingly positioned alongside branded alternatives, supported by improved packaging, consistent quality standards, and strategic shelf placement. Private labels are gaining consumer trust due to their value proposition, particularly in price-sensitive segments and during periods of economic uncertainty. Retailers are also expanding product assortments under private labels, including organic and premium variants, further strengthening their market presence and influencing purchasing behavior.

Technological Advancements in Packaging

Packaging innovation is enhancing product differentiation, safety, and convenience. BPA-free internal coatings are being widely adopted to address health concerns associated with traditional can linings. Easy-open lids, resealable formats, and lightweight can designs are improving usability and reducing material consumption. Manufacturers are also focusing on recyclable and eco-friendly materials to meet sustainability targets and regulatory requirements. Advances in aseptic and vacuum-sealing technologies are improving product shelf life while maintaining flavor, texture, and nutritional content. These innovations are enabling manufacturers to optimize logistics, reduce spoilage, and expand distribution across diverse geographic markets.

Growth of the Foodservice Industry

The global expansion of quick-service restaurants, cloud kitchens, catering services, and institutional food providers is significantly increasing demand for canned vegetables. These products offer standardized quality, consistent taste, and reliable supply, which are critical for large-scale food operations. Reduced preparation time, minimal waste, and ease of storage make canned vegetables a cost-efficient ingredient choice for foodservice operators. Bulk packaging formats further support high-volume usage, while extended shelf life reduces inventory risks. As foodservice businesses continue to scale and diversify menus, demand for versatile and ready-to-use vegetable ingredients is expected to remain strong.

Evolution of a Convenience Food Segment

Canned vegetables are a key component of the broader convenience food ecosystem, offering year-round availability of seasonal produce and reducing dependency on fresh supply chains. They contribute to lower food waste by extending product usability and enabling portion control. The segment is evolving with the introduction of value-added products such as pre-seasoned vegetables, ready-to-cook meal kits, and blended vegetable combinations designed for specific recipes. Premiumization is also evident, with increased availability of organic, specialty, and region-specific vegetable variants. These developments are expanding the category beyond basic staples to include differentiated offerings that cater to diverse consumer preferences and usage occasions.

Top Trends in the Canned Vegetables Market

- Health-oriented product reformulation: Manufacturers are actively reformulating products by reducing sodium content, eliminating artificial preservatives, and minimizing added sugars to meet regulatory standards and dietary guidelines. There is also increased focus on retaining micronutrients during processing, along with the introduction of organic-certified and non-GMO variants. These changes are particularly relevant in mature markets where label scrutiny and health-driven purchasing decisions are high.

- Sustainability and circular packaging: Companies are transitioning toward fully recyclable metal cans, BPA-free linings, and reduced material usage to improve environmental performance. Lifecycle assessments and carbon footprint reduction strategies are being integrated into packaging design. In addition, brands are adopting circular economy practices, including recycled input materials and improved waste management systems, to align with regulatory requirements and retailer sustainability benchmarks.

- Convenience-driven consumption patterns: Demand is increasing for ready-to-use vegetables that eliminate washing, cutting, and preparation time. This trend is driven by time-constrained consumers, particularly in urban households. Portion-controlled packaging, easy-open formats, and pre-seasoned variants are further enhancing usability, making canned vegetables suitable for both quick home cooking and semi-prepared meal solutions.

- Growth of private label penetration: Retailers are expanding private label portfolios with improved product quality, consistent supply, and competitive pricing strategies. These products are increasingly positioned alongside branded offerings, supported by better packaging design and quality assurance. The shift is enabling retailers to strengthen margins while providing consumers with cost-effective alternatives, especially during periods of price sensitivity.

- Expansion of e-commerce grocery platforms: Online grocery platforms are increasing accessibility to a wider range of canned vegetable products, including bulk packs and niche variants. Subscription-based purchasing, automated reordering, and bundled offerings are improving repeat sales. Digital channels also allow for targeted promotions, price comparisons, and consumer reviews, influencing purchasing behavior and accelerating adoption.

- Premiumization and product diversification: The canned vegetables industry is witnessing the introduction of premium offerings such as organic vegetables, specialty imports, and value-added products like seasoned mixes and ready-to-cook blends. These products cater to higher-income consumers seeking quality differentiation, convenience, and enhanced flavor profiles. Product diversification is also expanding into ethnic and region-specific vegetable varieties to address diverse culinary preferences.

Canned Vegetables Market Segmental Insights

By Product Type

Based on product type, the canned vegetables market share is segmented into canned peas, tomatoes, corn, beans, mushrooms, and others. The tomatoes segment dominated in 2025 due to its extensive application across retail consumption and industrial food processing.

- Tomatoes: Includes diced, crushed, peeled, whole, and paste formats used extensively in sauces, soups, ready meals, and foodservice operations. High usage frequency, consistent demand from processed food manufacturers, and versatility across cuisines contribute to its leading market share.

- Peas: Widely consumed due to affordability, nutritional value, and ease of use. Strong demand exists across both household cooking and institutional foodservice applications, supported by stable supply and low price volatility.

- Corn: Used in salads, soups, side dishes, and packaged foods. Demand remains steady due to broad consumer acceptance and its role as both a standalone product and an ingredient in mixed vegetable offerings.

- Beans: Includes green beans and other variants, offering high fiber content and versatility in meal preparation. Commonly used in both traditional and modern recipes, supporting consistent demand across regions.

- Mushrooms: Increasingly utilized in ready-to-eat meals, sauces, and premium food products. Growth is supported by demand from foodservice operators and rising consumer preference for diverse ingredient options.

- Others: Includes carrots, spinach, mixed vegetables, and specialty blends. These products cater to convenience-driven consumption and are often positioned as ready-to-cook solutions for complete meals.

By Packaging Type

The market for canned vegetables is segmented into metal cans, glass jars, and others, with metal cans maintaining dominance due to cost efficiency and product protection.

- Metal cans: Provide airtight sealing, resistance to light and oxygen, and extended shelf life. Their durability and stackability support efficient transportation and storage, making them the preferred format for both manufacturers and retailers.

- Glass jars: Positioned as premium packaging due to product visibility, reusability, and perceived quality. Often used for specialty or high-value products, appealing to consumers seeking transparency and higher-grade offerings.

- Others: Includes flexible pouches and alternative formats that focus on portability, reduced material usage, and ease of disposal. These formats are gaining traction in niche segments and on-the-go consumption categories.

By Distribution Channel

The market is segmented into supermarkets & hypermarkets, convenience stores, online retail, and others.

- Supermarkets & hypermarkets: Remain the dominant channel due to extensive shelf space, product variety, and promotional activities. Bulk purchasing options and strong brand visibility contribute to high sales volumes.

- Convenience stores: Cater to immediate consumption needs and smaller purchase quantities. Their proximity and accessibility make them relevant in urban and semi-urban areas.

- Online retail: Expanding rapidly with increasing digital adoption. Offers price transparency, wider assortment, and doorstep delivery, supporting growth in both urban and emerging markets.

- Others: Includes wholesale distribution, institutional supply, and direct procurement by foodservice operators, supporting large-volume transactions and consistent demand.

By End Use

The market is segmented into household and foodservice applications, with both segments contributing significantly to overall demand.

- Household: Accounts for the largest share due to widespread adoption of convenient, long-lasting food products. Demand is driven by ease of storage, minimal preparation requirements, and suitability for daily cooking.

- Foodservice: Growing steadily as restaurants, catering services, and institutional kitchens require consistent, pre-processed ingredients. Bulk packaging and standardized quality make canned vegetables suitable for large-scale operations.

| By Product Type | By Packaging Type | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America accounted for 34.2% of the global canned vegetables market share in 2025, supported by high consumption of processed and packaged foods.

- The United States dominates due to established food processing industries, high demand for convenience foods, and strong retail penetration.

- Private label expansion and price competitiveness are influencing purchasing behavior across major retail chains.

- Advanced logistics and cold chain alternatives enable efficient distribution and consistent product availability.

Europe

Europe’s canned vegetables industry was valued at USD 8.5 billion in 2025 and continues to show stable growth.

- Demand is influenced by sustainability regulations, clean-label preferences, and high consumer awareness regarding food sourcing.

- Countries such as Germany, France, and the UK lead regional consumption due to strong retail infrastructure.

- Private label products dominate shelf space, supported by retailer-driven pricing strategies.

Asia Pacific

Asia Pacific is the fastest-growing regional market due to rapid urbanization and evolving consumption patterns.

- China and India are key contributors, supported by increasing disposable incomes and expanding middle-class populations.

- Growth in modern retail formats and e-commerce platforms is improving product accessibility.

- Changing dietary habits and rising awareness of convenience foods are accelerating adoption.

LATAM

Latin America and the Middle East are emerging markets with increasing demand for affordable and long-lasting food products.

- Brazil and Mexico lead regional demand due to urban population growth and price-sensitive consumption patterns.

- In the Middle East, reliance on imports and expansion of foodservice infrastructure are key growth drivers.

Canned Vegetables Market Share

- The market remains moderately fragmented, with top players accounting for approximately 48% of global revenue in 2025.

- Leading companies leverage scale, distribution networks, and brand recognition to maintain a competitive advantage.

- Private label brands are intensifying competition, particularly in developed markets.

- Regional players are focusing on localized offerings and cost competitiveness to expand market presence.

Top Companies in the Canned Vegetables Market

- Del Monte Foods

- Conagra Brands

- Bonduelle Group

- Green Giant

- Kraft Heinz Company

- Dole Food Company

- General Mills

- B&G Foods

- Seneca Foods Corporation

- Ardo Group

- Princes Group

- Campbell Soup Company

- Del Monte Foods focuses on broad product portfolios and global distribution to maintain market leadership.

- Conagra Brands emphasizes innovation and premium offerings to meet evolving consumer preferences.

- Bonduelle Group invests in sustainability and plant-based product expansion.

- Kraft Heinz Company leverages strong brand equity and large-scale manufacturing capabilities.

Canned Vegetables Market News:

- In April 2025, Conagra Brands indicated potential price adjustments across its canned food portfolio, including vegetables, in response to rising input costs and tariffs on tin mill steel used in packaging. This reflects increasing cost pressures and margin management challenges within the canned food industry.

- In July 2025, Del Monte Foods filed for Chapter 11 bankruptcy protection, highlighting structural challenges across the packaged food sector, including shifting consumer preferences toward fresh and private label alternatives, as well as elevated production and distribution costs.

Frequently Asked Questions

How big is the global canned vegetables market?

As per Zeal Market Research, the global canned vegetables market was valued at USD 32.4 billion in 2025 and is projected to increase from USD 34.1 billion in 2026 to reach USD 45.8 billion by 2031, with a CAGR of 6.1% during the forecast period (2026-2031).

What is driving growth in the global market?

Growth is driven by increasing demand for convenience foods, extended shelf-life products, rising urbanization, expansion of modern retail and e-commerce channels, and growing reliance on ready-to-use cooking ingredients across households and foodservice sectors.

Which products are most popular in the global market?

Popular products include canned tomatoes, corn, peas, beans, mushrooms, and mixed vegetables, widely used in sauces, soups, ready meals, and everyday cooking applications.

Which regions are leading the global market?

North America leads the market due to strong consumption of processed foods and established retail infrastructure, while Europe maintains steady demand and Asia-Pacific is the fastest-growing region driven by urbanization and income growth.

Who are the leading players in the canned vegetables market?

Leading companies operating in the canned vegetables market include Del Monte Foods, Conagra Brands, Bonduelle Group, Kraft Heinz Company, Green Giant, Dole Food Company, and B&G Foods.