Canned Tomatoes Market Size

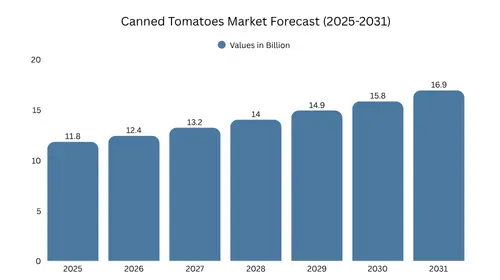

According to Zeal Market Research, the global canned tomatoes market size was valued at USD 11.8 billion in 2025 and is projected to grow from USD 12.4 billion in 2026 to reach USD 16.9 billion by 2031, registering a CAGR of 6.4% during the forecast period (2026-2031). Market growth is primarily supported by rising global demand for shelf-stable food ingredients, increasing household preference for convenient cooking solutions, and expanding use of tomato-based products across restaurants, catering services, and packaged food manufacturing.

Key Market Insights

- Europe accounted for the leading regional share of the global canned tomatoes market at 34.2% in 2025, supported by strong tomato cultivation, advanced processing infrastructure, and high domestic as well as export demand.

- By product type, the whole peeled tomatoes segment led the market in 2025 with 31.5% of global revenue, equivalent to approximately USD 3.7 billion, driven by premium culinary positioning and strong use in sauces, soups, and restaurant kitchens.

- By packaging type, metal cans remained the dominant category owing to durability, cost efficiency, barrier protection, and established global recycling systems.

- By distribution channel, supermarkets and hypermarkets continued to lead sales as consumers prefer one-stop grocery shopping, bulk buying, and access to multiple brands and private label products.

- The foodservice segment is projected to record the fastest growth among end users, supported by the expansion of pizza chains, pasta restaurants, hotels, institutional kitchens, and ready-meal manufacturers.

What are the growth opportunities in the Canned Tomatoes market?

Expansion Across Emerging Markets

One of the key growth opportunities is emerging across developing regions, where demand for packaged and shelf-stable vegetables continues to increase. This broader shift is supporting steady expansion in the canned vegetables segment, driven by rapid urbanization, rising disposable incomes, and the growth of modern retail across Asia Pacific, Latin America, and the Middle East.

Canned tomatoes are benefiting directly from this trend, offering a reliable and cost-effective alternative to fresh produce, particularly in regions where cold-chain infrastructure is limited and seasonal supply remains inconsistent.

Premium and Health-Focused Product Innovation

Manufacturers are increasingly launching premium canned tomato products, including organic, no-added-salt, vine-ripened, sun-ripened, and specialty regional varieties. Consumers are also showing rising interest in clean-label food products with fewer preservatives and transparent sourcing. Premiumization enables brands to improve margins while appealing to health-conscious and quality-driven buyers.

Foodservice and Bulk Packaging Demand

The rapid growth of restaurants, catering companies, institutional kitchens, and quick-service chains presents a major opportunity for bulk canned tomato formats. Foodservice buyers value consistent taste, standardized quality, labor savings, and reduced preparation time. Large-volume cans and industrial packs are increasingly used for pizza sauces, curries, soups, stews, and ready-to-eat meal production.

Sustainable Packaging Development

Sustainability is becoming a long-term growth driver across the industry. Producers are investing in recyclable steel packaging, lightweight cans, renewable energy processing facilities, and water-efficient farming practices. BPA-free can linings and environmentally responsible packaging are also helping brands strengthen retailer partnerships and consumer trust.

Digital Grocery and Private Label Growth

E-commerce grocery platforms and retailer-owned brands are opening new avenues for expansion. Online grocery purchases encourage pantry stocking behavior, while private-label canned tomatoes offer attractive pricing and growing quality acceptance. Retail chains are increasingly using private-label tomato categories to improve margins and customer retention.

Canned Tomatoes Market Trends

- Strong pantry staple demand: Consumers continue to view canned tomatoes as an essential ingredient for soups, sauces, pasta dishes, curries, casseroles, and stews. Their long shelf life, stable pricing relative to fresh seasonal tomatoes, and ease of storage support frequent repeat purchases across households, restaurants, and institutional kitchens.

- Organic and clean-label positioning: Demand is increasing for products labeled organic, preservative-free, non-GMO, low-sodium, and vine-ripened, particularly in North America and Europe. Health-conscious consumers are increasingly reviewing ingredient labels and preferring minimally processed products with transparent sourcing claims.

- Private label expansion: Major retailers are strengthening store-brand canned tomato portfolios through competitive pricing, improved packaging design, and broader product ranges. Private label growth is particularly strong during inflationary periods when consumers shift toward value-oriented grocery purchases without compromising core pantry staples.

- Premium culinary variants: Fire-roasted tomatoes, San Marzano-style tomatoes, seasoned blends, peeled plum tomatoes, and specialty Italian products are gaining shelf space. These products appeal to consumers seeking restaurant-style cooking outcomes, stronger flavor profiles, and premium recipe ingredients.

- Foodservice volume growth: Restaurants, pizza chains, hotels, cafes, and catering businesses are increasing procurement of canned tomatoes for a reliable year-round supply, consistent taste, and reduced preparation time. Bulk purchasing demand is especially strong for sauces, soups, pasta, and ready-meal applications.

- Packaging innovation: Easy-open lids, BPA-free linings, stack-efficient formats, lightweight cans, and recyclable packaging materials are becoming key product differentiators. Producers are also investing in improved labeling and shelf-ready packaging to enhance retail visibility and logistics efficiency.

Segmental Insights

By Product Type

Based on product type, the canned tomatoes industry is segmented into whole peeled tomatoes, diced tomatoes, crushed tomatoes, tomato puree, paste, and others. The whole peeled tomatoes segment led the global canned tomatoes market in 2025, accounting for 31.5% of global revenue, equivalent to approximately USD 3.7 billion, due to superior texture retention, premium perception, strong flavor quality, and versatility across household, restaurant, and industrial cooking applications.

- Whole Peeled Tomatoes: Widely preferred for pasta sauces, slow-cooked recipes, soups, stews, and premium restaurant dishes. Their intact structure allows users to crush or blend as needed, making them highly versatile. This segment commands stronger pricing in many retail markets.

- Diced Tomatoes: Popular for quick meal preparation, stews, curries, tacos, casseroles, and salsa-based recipes. Pre-cut convenience, consistent cube sizing, and reduced preparation time support strong household and foodservice demand.

- Crushed Tomatoes: Extensively used in pizza sauces, pasta bases, soups, and packaged food manufacturing, where smooth consistency and strong tomato flavor are required. This segment benefits from high-volume commercial usage.

- Tomato Puree: Common in concentrated cooking applications, ready-made sauces, gravies, and industrial formulations due to its thicker texture and richer flavor profile. It is widely used where faster sauce preparation is required.

- Paste: Used in industrial food processing, seasoning bases, marinades, ketchup manufacturing, and household cooking for flavor concentration. Tomato paste offers strong shelf life because of its compact format.

- Others: Includes cherry tomatoes, stewed tomatoes, flavored tomatoes, organic variants, and regional specialty products targeted at niche culinary demand.

By Packaging Type

Based on packaging type, the canned tomatoes industry is segmented into metal cans, cartons, jars, and others. Metal cans dominated in 2025 due to product safety, long shelf life, strong barrier protection, efficient transport economics, and widespread consumer familiarity across global grocery markets.

- Metal Cans: Leading segment supported by durability, resistance to contamination, light protection, strong shelf stability, and recycling advantages. Metal cans remain preferred for mainstream retail and bulk foodservice supply.

- Cartons: Growing in premium and sustainability-focused channels due to lighter weight, efficient storage, and easier handling. Carton formats are increasingly used for puree and crushed tomato products.

- Jars: Used mainly in premium retail segments where visibility, perceived freshness, and reusable packaging influence buying decisions. Glass jars are common in specialty sauces and gourmet tomato products.

- Others: Includes pouches, institutional packs, bag-in-box formats, and foodservice bulk containers designed for commercial kitchens and industrial processors.

By Distribution Channel

Based on distribution channel, the market is segmented into supermarkets & hypermarkets, convenience stores, online retail, wholesalers, and others. Supermarkets & hypermarkets remained the leading channel due to strong shelf visibility, broad assortment variety, promotional activity, and frequent grocery traffic.

- Supermarkets & Hypermarkets: Major sales channel driven by promotional pricing, multi-brand presence, private label offerings, and bulk purchasing behavior. Consumers often purchase canned tomatoes during routine monthly grocery trips.

- Convenience Stores: Important for small-format urban purchases, emergency grocery needs, and single-can buying behavior. This channel is relevant in densely populated cities.

- Online Retail: Fast-growing segment supported by grocery apps, subscription orders, pantry restocking trends, and price comparison convenience. Multipack sales are particularly strong online.

- Wholesalers: Critical for restaurants, institutional kitchens, hotels, caterers, and independent retailers purchasing in large volumes.

- Others: Includes specialty food stores, discount retailers, club stores, and direct distributor sales to commercial buyers.

By End Use

Based on end use, the global industry is segmented into household, foodservice, and industrial processing. The foodservice segment is expected to witness the fastest growth due to increasing restaurant expansion, rising global consumption of tomato-based menus, and growing demand for consistent ingredient sourcing.

- Household: Largest user base supported by routine cooking demand, pantry stocking habits, convenience needs, and year-round use in home recipes.

- Foodservice: Fast-growing segment driven by pizza chains, pasta outlets, cafes, hotels, caterers, cloud kitchens, and institutional meal providers requiring dependable supply and flavor consistency.

- Industrial Processing: Used in sauces, soups, ready meals, frozen foods, snacks, and packaged food manufacturing, where standardized quality and scalable input sourcing are essential.

Regional Insights

Europe

Europe accounted for 34.2% of the global canned tomatoes market share in 2025, making it the largest regional market. The region benefits from strong agricultural output, advanced tomato processing infrastructure, export competitiveness, and deeply rooted culinary demand.

- Italy is a global leader in premium canned tomato exports, supported by strong brand recognition, processing expertise, and demand for Italian-origin products.

- Spain and Portugal remain major industrial processors supplying both domestic and export markets through large-scale agricultural production.

- Germany, France, and the UK represent strong consumer markets with rising demand for organic, premium, and convenience-oriented tomato products.

North America

North America’s canned tomatoes industry was valued at USD 3.1 billion in 2025 and is expected to grow steadily through 2031. Stable demand is supported by packaged food consumption, strong retail infrastructure, and broad use of tomato-based meals.

- The United States dominates regional demand due to high packaged food consumption and strong household pantry stocking habits.

- Private label brands, warehouse retail formats, and discount grocery chains are supporting high-volume sales.

- Foodservice demand from pizza, pasta, soups, ready meals, and institutional catering remains significant.

Asia Pacific

The Asia Pacific region is among the fastest-growing markets globally. Rising incomes, changing diets, retail modernization, and western cuisine adoption are strengthening long-term category demand.

- China and India are witnessing rising demand through urbanization, modern grocery expansion, and increasing consumption of pasta, pizza, and sauce-based foods.

- Japan, South Korea, and Australia represent developed packaged food markets with higher premium product demand and strong convenience food consumption.

- E-commerce grocery channels are accelerating market penetration, especially in urban centers.

LATAM

Latin America and the Middle East are emerging as high-potential markets. Growth is supported by expanding supermarkets, rising hospitality demand, and increasing packaged food consumption.

- Brazil and Mexico are leading markets supported by modern retail growth, urban demand expansion, and growing foodservice sectors.

- Middle Eastern demand is increasing through hospitality, tourism, restaurant expansion, and rising demand for imported packaged food products.

Canned Tomatoes Market Share

- The top 5 players in the global market including, Conagra Brands, Del Monte Foods, Mutti, Cento Fine Foods, and Kraft Heinz collectively accounted for approximately 49% of global canned tomatoes sales in 2025, reflecting a moderately consolidated market structure.

- Large multinational brands benefit from sourcing scale, retailer relationships, and efficient distribution networks.

- Private label suppliers are intensifying price competition across mass-market channels.

- Premium European brands compete through quality positioning, origin branding, and product authenticity.

- Raw tomato price volatility, weather conditions, and freight costs remain key competitive variables.

Top Companies in the Canned Tomatoes Industry

Most prominent players operating in the canned tomatoes industry include:

- Conagra Brands

- Del Monte Foods

- Mutti

- Cento Fine Foods

- Kraft Heinz

- Hunt’s

- Napolina

- Cirio

- Red Gold

- La Doria

- Princes Group

- Pastene

- Goya Foods

- Pacific Coast Producers

- Simpson Imports

- Mutti is recognized for premium Italian tomato products and strong export positioning.

- Del Monte Foods benefits from broad grocery penetration and diversified canned food categories.

- Kraft Heinz leverages global retail relationships and strong packaged food branding.

- Conagra Brands maintains scale advantages through multi-category grocery operations.

- La Doria is a major private-label manufacturing supplier in Europe.

Canned Tomatoes Market News:

- In May 2026, Mutti announced its participation at TuttoFood 2026, where the company showcased premium Italian tomato products and highlighted its ongoing international expansion strategy across retail and foodservice channels.

Frequently Asked Questions

How big is the global canned tomatoes market?

According to Zeal Market Research, the global canned tomatoes market was valued at USD 11.8 billion in 2025 and is projected to increase from USD 12.4 billion in 2026 to reach USD 16.9 billion by 2031, registering a CAGR of 6.4% during the forecast period (2026-2031).

What is driving growth in the global market?

Growth is being driven by rising demand for shelf-stable food products, increasing household preference for convenient cooking ingredients, expanding restaurant consumption of tomato-based meals, and growing packaged food production worldwide.

Which products are most popular in the global market?

Popular products include whole peeled tomatoes, diced tomatoes, crushed tomatoes, tomato puree, tomato paste, fire-roasted tomatoes, and specialty seasoned canned tomato variants.

Which regions are leading the global market?

Europe leads the market due to strong tomato cultivation, advanced processing infrastructure, and export leadership, while North America and Asia-Pacific are also witnessing steady growth.

Who are the leading players in the canned tomatoes market?

Leading companies operating in the canned tomatoes market include Mutti, Del Monte Foods, Conagra Brands, Kraft Heinz, Cento Fine Foods, Red Gold, La Doria, and Hunt’s.