Canned Peas Market Size

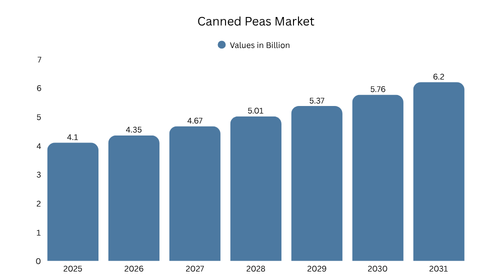

The global canned peas market size was valued at USD 4.1 billion in 2025 and is projected to grow from USD 4.35 billion in 2026 to reach USD 6.2 billion by 2031, registering a CAGR of 7.3% during the forecast period (2026-2031). This growth is driven by the increasing role of peas as a mid-tier plant protein within global nutrition systems, expansion of shelf-stable food consumption aligned with food loss reduction policies, and growing adoption across institutional and foodservice supply chains. The canned peas market is further supported by its integration into climate-smart agriculture frameworks, where legumes contribute to sustainable food systems through nitrogen fixation, reduced fertilizer dependency, and improved soil productivity.

In addition, canned peas serve as a reliable supply-side stabilizer within global food systems, ensuring year-round availability independent of harvest cycles. Their long shelf life reduces dependency on cold-chain infrastructure, enabling penetration into emerging and infrastructure-constrained markets while supporting bulk procurement strategies across public and private sectors.

Key Market Insights

- Europe accounted for the leading regional share of the global canned peas market at 36.9% in 2025, supported by strong domestic cultivation, advanced processing infrastructure, and high per capita consumption of preserved vegetables.

- By product type, standard green peas led the market in 2025 with 68.4% of global revenue, equivalent to approximately USD 2.8 billion, driven by their role as a staple ingredient across both household cooking and industrial food preparation.

- By processing type, conventional thermal processing dominated due to scalability and cost efficiency, although nutrient-retention technologies are emerging as a competitive differentiator.

- By distribution channel, supermarkets and hypermarkets held the largest share, while institutional and bulk procurement channels are expected to expand faster due to increasing demand from public food programs and large-scale catering systems.

- The foodservice and institutional segment is projected to record the fastest growth, supported by portion standardization, reduced preparation time, and minimal food waste.

- Private label penetration remains high across developed markets, intensifying price competition and reinforcing commodity-like characteristics in standard product categories.

What are the growth opportunities in the canned peas market?

Nutrient-Retention Processing Innovation

One of the most prominent growth opportunities lies in advancing processing technologies that minimize nutrient degradation. Thermal canning has been shown to reduce certain nutrients such as antioxidants and protein quality. This creates a strong opportunity for manufacturers to adopt optimized sterilization processes, controlled heat exposure techniques, and improved packaging systems to retain nutritional integrity. Positioning products as “nutrient-preserved” or “optimized nutrition” variants can enable premium pricing and differentiation in an otherwise commoditized market.

Circular Economy and Full Biomass Utilization

Pea processing generates significant by-products including pods and residues, which are rich in protein and suitable for animal feed, protein extraction, and bio-based material applications. Integrating full biomass utilization into production systems enables manufacturers to reduce waste, improve resource efficiency, and diversify revenue streams. This approach aligns with circular economy models and supports sustainability-driven procurement policies.

Integration into Climate-Smart and Sustainable Diet Systems

Canned peas present a strong opportunity within climate-smart agriculture frameworks. As nitrogen-fixing crops, peas improve soil fertility and reduce reliance on synthetic fertilizers, lowering environmental impact. Their shelf-stable format allows them to be incorporated into institutional food systems, contributing to low-carbon diet infrastructure and long-term sustainability initiatives led by governments and international organizations.

Regulation-Enabled Product Diversification

Food standards permit the addition of seasonings, fats, and other ingredients within defined limits, enabling manufacturers to develop flavored, enriched, and mixed canned pea products. This regulatory support allows for scalable product innovation without compromising compliance, creating opportunities to expand into ready-to-eat and convenience-oriented segments while maintaining operational efficiency.

Expansion in Institutional Nutrition and Food Security Programs

Canned peas are increasingly integrated into public nutrition programs due to their affordability, nutrient density, and long shelf life. Their role as a mid-tier protein source makes them suitable for school feeding programs, emergency food reserves, and large-scale distribution systems. This creates a stable, policy-driven demand stream that is less sensitive to retail market fluctuations.

Canned Peas Market Trends

- Shift toward climate-smart legumes: Increasing emphasis on sustainable agriculture is driving adoption of peas as nitrogen-fixing crops that enhance soil health and reduce fertilizer input requirements.

- Regulation-driven product innovation: Standardized food regulations are enabling development of seasoned, enriched, and mixed canned pea products, supporting structured and scalable innovation.

- Positioning as nutrition system components: Canned peas are being integrated into balanced diet frameworks due to their protein, fiber, and micronutrient content, particularly in cost-sensitive markets.

- Alignment with food loss reduction strategies: Shelf-stable processing reduces post-harvest losses and ensures consistent food availability throughout the year.

- Expansion of institutional demand: Growing use in schools, hospitals, and large-scale catering systems is increasing demand for standardized and efficient food inputs.

- Processing and packaging advancements: Improvements in can linings, sterilization techniques, and preservation methods are enhancing product safety and shelf stability.

- Shift toward value-added formats: Increasing availability of flavored and ready-to-eat canned peas is transforming the category from a basic ingredient to a convenience food solution.

Segmental Insights

By Product Type

Based on product type, the market for canned peas is segmented into standard green peas, organic peas, and value-added/seasoned peas. The standard green peas segment led the market in 2025, accounting for 68.4% of global revenue due to affordability and extensive application across multiple end-use sectors.

- Standard Green Peas: The dominant segment driven by consistent demand across households, foodservice, and industrial processing. High volume consumption and cost efficiency support its leading position.

- Organic Peas: Growing segment supported by demand for clean-label, chemical-free, and sustainably produced food products, particularly in developed markets.

- Value-Added/Seasoned Peas: Includes flavored, spiced, and mixed variants enabled by regulatory frameworks, offering higher margins and catering to convenience-driven consumption patterns.

By Processing Type

Based on processing type, the canned peas industry is segmented into conventional thermal processing and advanced nutrient-optimized processing techniques.

- Conventional Processing: Widely adopted due to established infrastructure, scalability, and lower production costs, making it the industry standard.

- Advanced Processing: Focuses on preserving nutritional content and improving product quality through controlled heat treatment and innovative preservation technologies.

By Distribution Channel

Based on distribution channel, the market is segmented into supermarkets & hypermarkets, online retail, institutional/bulk supply, and others.

- Supermarkets & Hypermarkets: The leading channel supported by strong retail presence, product visibility, and consumer accessibility.

- Online Retail: Expanding rapidly due to increased adoption of e-commerce platforms and convenience-driven purchasing behavior.

- Institutional/Bulk Supply: Includes government programs, educational institutions, healthcare facilities, and large-scale catering services requiring high-volume procurement.

- Others: Includes local retail outlets and specialty food stores catering to regional demand patterns.

By End Use

Based on end use, the global market is segmented into household consumption, foodservice, and industrial processing.

- Household Consumption: The largest segment driven by routine cooking applications and the need for convenient, shelf-stable ingredients.

- Foodservice: The fastest-growing segment due to demand for consistent quality, portion control, and reduced preparation time.

- Industrial Processing: Includes usage in packaged foods such as soups, ready meals, and frozen dishes, supporting large-scale food manufacturing.

| By Product Type | By Processing Type | By Distribution Channel | By End Use |

|---|---|---|---|

|

|

|

|

Regional Insights

Europe

Europe accounted for 36.9% of the global canned peas market share in 2025, making it the largest regional market.

- Countries such as France, the UK, and Italy dominate due to strong consumption of preserved vegetables and established canning industries.

- High agricultural productivity and efficient supply chains support consistent raw material availability.

- Regulatory focus on sustainability and food quality standards influences product development and innovation.

North America

North America canned peas market was valued at USD 1.1 billion in 2025 and is expected to grow steadily through 2031.

- The United States leads due to high consumption of convenience foods and strong institutional demand.

- Public nutrition programs and foodservice adoption contribute to stable demand patterns.

- Product innovation focuses on low-sodium, clean-label, and nutrient-enhanced offerings.

Asia Pacific

The Asia Pacific region is among the fastest-growing markets globally.

- India and China are key growth markets driven by urbanization and increasing demand for affordable nutrition.

- Limited cold-chain infrastructure supports adoption of shelf-stable canned vegetables.

- Government-led food security and nutrition initiatives are accelerating market expansion.

LATAM

Latin America and the Middle East are emerging as high-potential markets.

- Brazil and Mexico are leading markets supported by rising processed food consumption.

- In the Middle East, demand is driven by import dependency and the need for long shelf-life food products.

Canned Peas Market Share

- The market is moderately fragmented, with the top players accounting for approximately 45-50% of global revenue.

- High private label penetration intensifies price competition and limits product differentiation across standard segments.

- Commodity-like characteristics of canned peas create margin pressure for manufacturers.

- Companies are increasingly focusing on value-added products, sustainability initiatives, and processing innovation to differentiate.

Leading Companies in the Canned Peas Industry

Few of the prominent players operating in the canned peas market include:

- Nestlé S.A.

- Bonduelle Group

- Green Giant (B&G Foods)

- Del Monte Foods, Inc.

- Conagra Brands, Inc.

- Princes Group

- Ardo Group

- Kraft Heinz Company

- Orkla ASA

- Dole plc.

Latest Developments in the Canned Peas Market:

- In March 2026, Seneca Foods acquired the Green Giant U.S. frozen vegetable business from B&G Foods, reuniting Green Giant’s frozen and shelf-stable vegetable operations under a single company. The move is expected to strengthen procurement efficiencies, vegetable sourcing capabilities, and innovation across canned and frozen pea categories.

- In 2025, Greenyard continued expanding its sustainability and plant-based product initiatives across processed vegetables, including canned peas, focusing on environmentally efficient sourcing and value-added vegetable products aimed at convenience-oriented consumers.

Frequently Asked Questions

How big is the global canned peas market?

The global canned peas market was valued at USD 4.1 billion in 2025 and is projected to reach USD 6.2 billion by 2031, growing at a CAGR of 7.3% during the forecast period (2026-2031).

What is driving growth in the global market?

Growth is driven by the role of peas as a mid-tier protein source, alignment with food loss reduction policies, increasing institutional demand, and expansion of shelf-stable food consumption.

Which products are most popular in the global market?

Standard green peas dominate the market, followed by organic and value-added seasoned variants.

Which regions are leading the global market?

Europe leads the market, followed by North America, while Asia-Pacific is the fastest-growing region.

Who are the leading players in the canned peas market?

Leading companies include Bonduelle Group, Del Monte Foods, Conagra Brands, Green Giant, Nestlé S.A., and Princes Group.